As noted in a recent blog post, the Federal Reserve stopped accounting for its “M3” monetary aggregate in early 2006 – at a time when M3 growth was accelerating, and during a boom before the 2007-2009 bust.

M3 is, or was, one of the Federal Reserve’s “monetary aggregates.” The money supply doesn’t just include Federal Reserve Notes, like $100 bills. The Fed adds a progressively broader range of instruments to its measures of the “money supply,” which have ranged from the narrow M1 aggregate (demand deposits and cash) to M2 (adding things like savings deposits and money market mutual funds) to the broader M3 aggregate.

Announcing its decision to stop accounting for M3, the Fed stated that M3 hadn’t been providing information that wasn’t already in M2, and that it hadn’t been considered important in monetary policy.

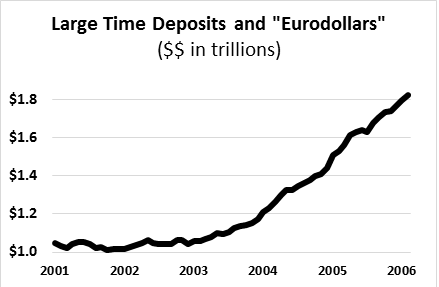

M3 was different than M2 because it added other “stuff” considered “money” that wasn’t already in M2. These included large time deposits (in excess of the historical $100,000 limit for deposit insurance) and the Fed’s counting of Eurodollars (in the Fed’s definition, dollar-denominated bank accounts in US banks outside the United States).

Big money. At the time the Fed stopped reporting M3, these two categories totaled nearly $2 trillion – and they had been growing rapidly in the three years leading up to their ‘dismissal’ from the money supply. Together, these two components mushroomed from mid-2003 to early 2006, rising over $700 billion.

But the Fed may have ‘dismissed’ them from the monetary aggregates right when they were getting important, during a housing finance bubble about to burst into the worst financial crisis since at least the Great Depression.

Why was this stuff growing so fast, at an accelerating pace, at a time when growth in M2 – the stuff that the Fed chose to keep reporting – was declining?

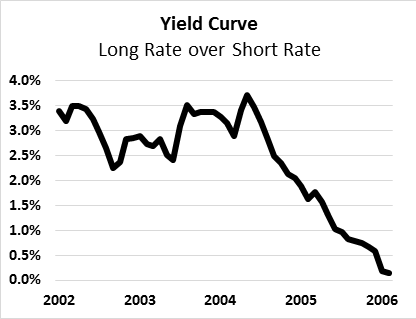

Financial and economic analysts are taught to respect the importance of watching something called the ‘yield curve.’ The ‘yield curve’ is often shown using the interest rates for Treasury securities, ranging from ‘short-term’ (one year or less “T-Bills”) up to long-term (for instance, 10 year T-bonds).

Normally, but not always, long-term rates are above short-term rates. The wider the spread, the wider the yield curve.

Other things equal, wider yield curves tend to be associated with higher incentives for bank lending and money growth, and in turn, economic stimulus. Narrow and/or narrowing yield curves, on the other hand, can represent ‘tighter’ (restrictive) monetary policy by the Federal Reserve, as the Fed effectively controls the short-end of the yield curve.

Here’s what was happening to long-term interest rates and short-term interest rates in the years leading up to the Fed’s decision to stop reporting M3. Short-term rates were rising significantly relative to long rates.

In turn, the spread – the difference between long rates and short rates – was falling significantly – consistent with the slowing growth in M2 at the time.

But why were large time deposits and Eurodollars ballooning in 2004-2006, even as M2 growth was falling with a narrowing yield curve?

Perhaps banks and/or the Fed found some innovative new methods for “money creation,” at least for the big money which ended up fueling the Big Bubble.

Longer story short – here’s a speculative hypothesis. Was the Fed’s “Fedwire” wire transfer system mined by enterprising banks as a way to effectively create money out of thin air, given the Fed’s liberal overdraft policies and end-of-minute accounting for overdraft positions, on a system that moved big money in seconds?

A speculation, perhaps worthy of exploration and/or investigation. There are some outlandish and possibly outrageous questions underneath, but in light of stories like this one from just a few weeks ago, perhaps we shouldn’t keep outlandish and possibly outrageous questions bottled up inside of us.