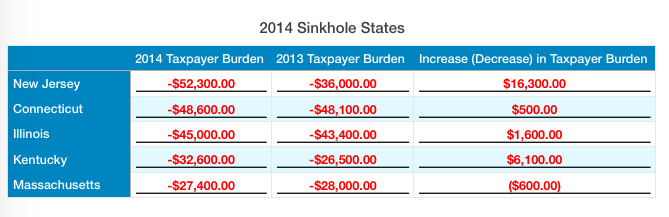

Five Sinkhole States Analysis

New Jersey became the state with the worst Taxpayer Burden because of a dramatic upsurge in its unfunded pension liabilities. This increase was a result of the application of the new pension standard, which takes into account that the state's major pension plans will run out of assets before all promised benefits are paid. Therefore the state will be liable to pay more pension contributions to offset the foregone investment income.

Kentucky moved back into the bottom five sinkhole states because it was also greatly affected by the new pension standards. While its Employees Retirement System was able to claim it won't run out of assets, its Teachers' Retirement System's unfunded liability increased because additional state contributions will need to be made into the plan when assets are expected to be depleted because of the new pension reform.

Illinois was not as adversely affected by the new pension standard because its two pension plans are not projected to run out of assets for 50 years. Furthermore, Connecticut and Massachusetts' pension plans are not expected to run out of assets before all benefits are paid. These projections don’t seem very realistic in light of the fact that these states have some of the most underfunded pensions in the country, with Illinois actually being the worst.

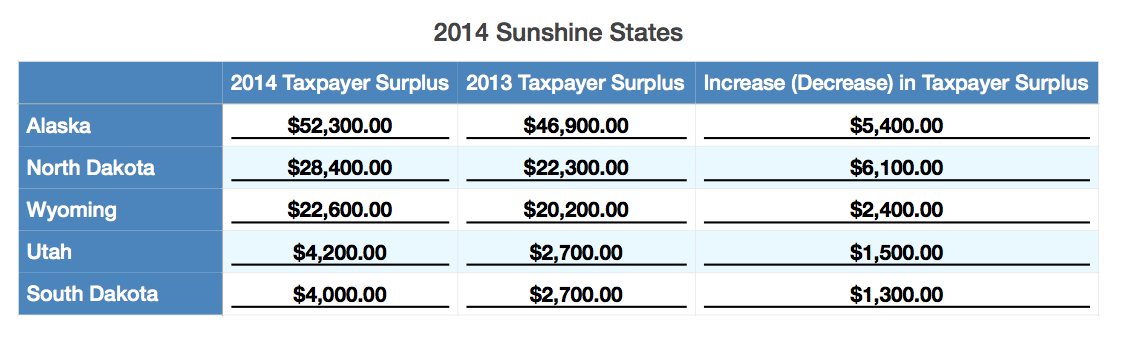

Five Sunshine States Analysis

Alaska's financial condition continued to improve in 2014. As shown in its financial statement, the state’s total net position rose by $7 billion, primarily due to an increase of $3.1 billion in interest and investment income (Alaska Department of Administration - Division of Finance, 2014). While Alaska's pension funds are not well-funded, the state does have more than enough unrestricted assets available to pay accrued pension benefits and all of its other bills. During 2014 these assets provided significant investment income..

The improvement in North Dakota's financial condition is largely due to the implementation of GASB Statement No. 67, which allows the state to revalue its pension plan assets using market value. As a result, these assets increased in value by an average of 29% over the state’s four pension plans. Significant increases in tax revenues during the year also contributed to North Dakota’s prosperity (North Dakota OMB - Fiscal Management Division, 2014).

TIA recognizes six other Sunshine States. These states have assets in excess of bills, including unfunded promises to state retirees. These states include Nebraska, Idaho, Oregon, Tennessee, Iowa, and Montana.

Taxpayer Burden Exists in 39 States

Balanced budget requirements should prevent state governments from shifting the financial burden for current-year services onto future-year taxpayers. True balanced budget accountability reduces elected officials' ability to incur costs without including them in current budget calculations. TIA’s study found 39 states have created Taxpayer Burdens through not truly balancing their budgets. These burdens will be the responsibility of future taxpayers.

The main reason for the creation of Taxpayer Burden is that full compensation costs, especially related to earned retirement benefits, were not included in prior budgets. Money that should have been set aside to provide for these costs was spent elsewhere. Therefore future taxpayers will have to pay for services and benefits that were received by prior taxpayers.

Evidence of these practices appears in state annual financial reports. As indicated in Appendix IV, nationwide TIA identified $628 billion of unfunded pension and $559 billion of unfunded retirees’ health care liabilities. As indicated in Appendix V, only $229 billion of these liabilities were reported on the face of state balance sheets. Collectively more than $956 billion of earned pension and health care benefits earned have not been included in prior state budgets and financial statements. Future taxpayers are responsible for all unfunded liabilities whether they appear on their state’s balance sheet or not.

Taxpayers are also ultimately responsible for unfunded promises on the part of the federal and local governments. For example, using the same methodology, citizens in Chicago have a Taxpayer Burden of $927,700 per taxpayer. Every Chicago taxpayer would have to write a check to their city for $28,200, to their state for $45,000, and to the U.S. Treasury for $850,00013 to cover government promises already made on their behalf.