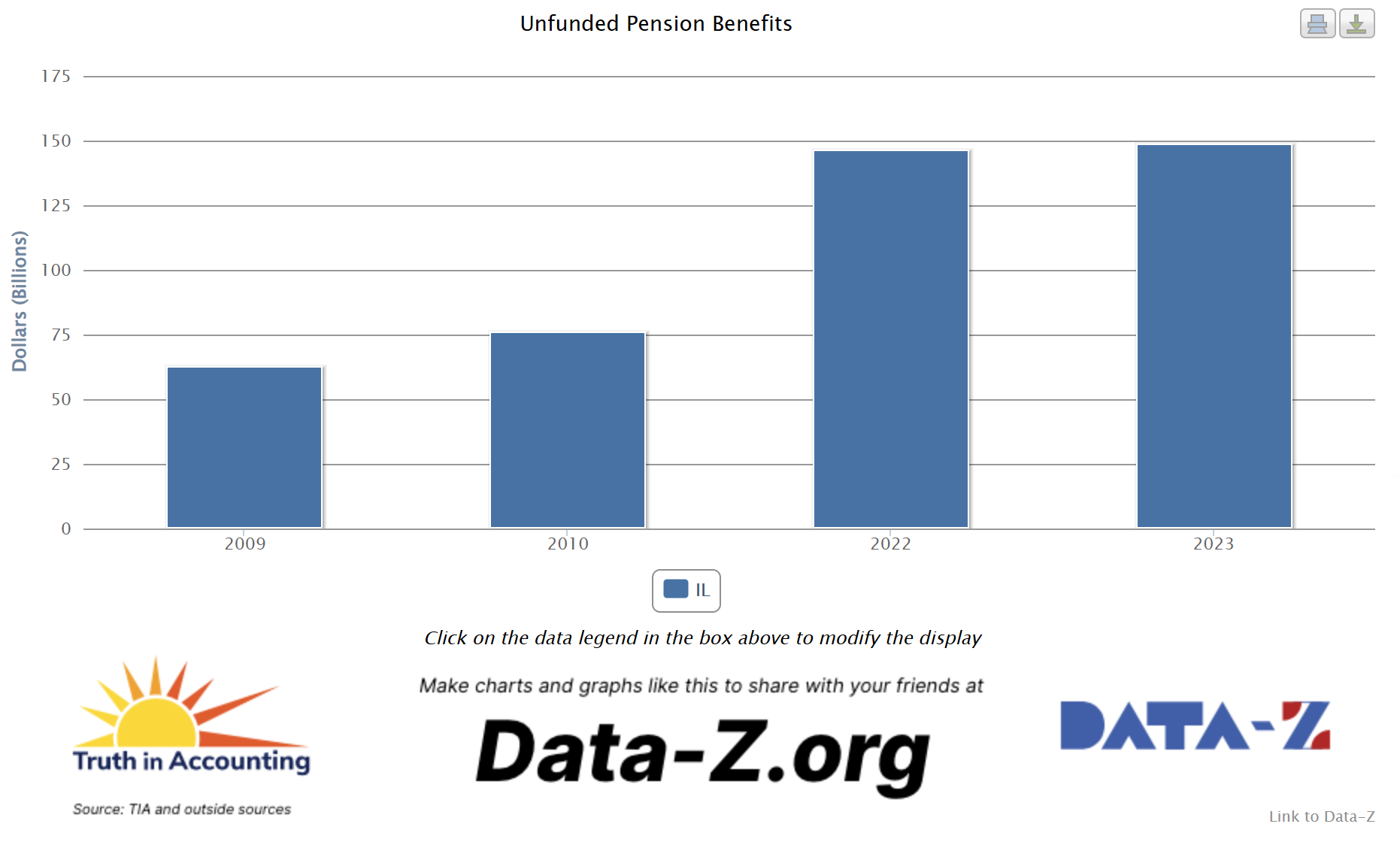

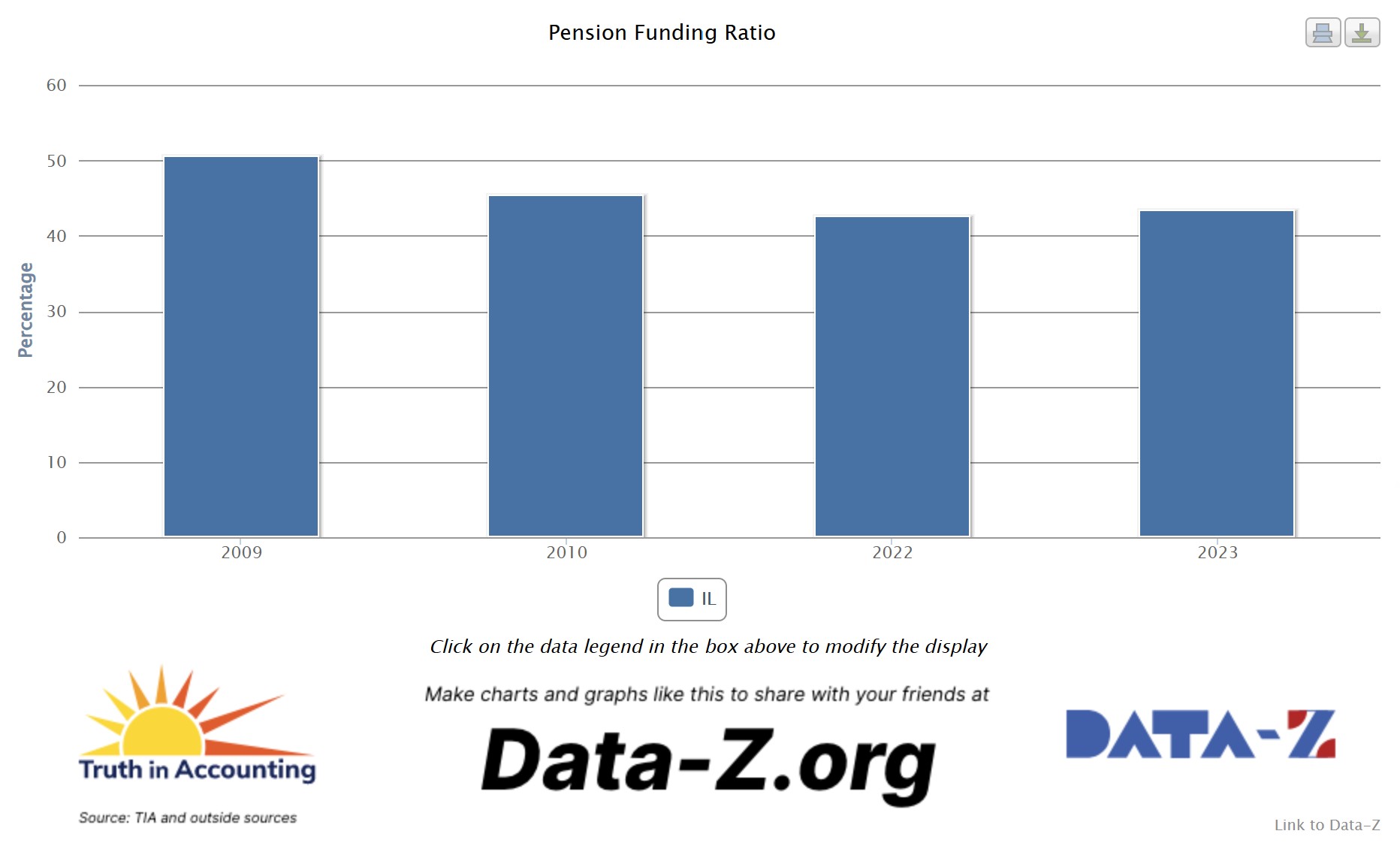

Illinois’ public pension systems are in severe crisis, with chronic underfunding threatening retirees, taxpayers, and the state’s fiscal stability. Truth in Accounting has reported on this issue for years, highlighting how the state’s failure to make full actuarially determined contributions (ADC) has exacerbated the problem. As of fiscal year 2024, Illinois’ pension systems face $148.6 billion in unfunded liabilities, with a funded ratio of just 47.8%. This is well below the 65% threshold considered critical under private sector pension funding standards established by federal law. Pension payments consume approximately 20% of the state budget, crowding out investments in education, infrastructure, and public services. Benefit increases without corresponding funding adjustments will worsen the state’s long-term pension imbalance.

Tier 2 Pensions: The Cost Control Reform Now Under Attack

In 2011, Illinois created Tier 2 pensions for workers hired after January 1 of that year. The reforms were a direct response to Tier 1’s unsustainable promises and were projected to save billions by slowing liability growth.

Now, some legislators, backed by public-sector unions, are pushing pension increases to roll back key Tier 2 protections. These proposals would make benefits far more generous, directly adding to the $148.6 billion unfunded hole.

Recent and Proposed Pension Benefit Increases

-

Chicago Police and Fire (Public Act 104-0065, signed August 2025): This benefit increase is estimated to cost the city more than $11 billion over 30 years. Chicago’s police and fire funds, already funded at 20–25% or less, saw their situations worsen dramatically. If similar legislation were passed for other cities and local governments around the state, their accrued benefits could increase by 43%, resulting in a substantial increase in pension costs.

-

Statewide Tier 2 Overhaul (SB 1937 / House Amendment 2 – “Fair Retirement and Recruitment Act”): This broader bill is expected to significantly increase pension costs, though a comprehensive actuarial estimate is not yet available. Estimates for a related Tier 2 proposal (HB 2540) range from $53 billion to as much as $80 billion or more over the coming decades across state and local systems. These increases could place additional pressure on property taxes and government services and benefits.

-

What These Enhancements Would Do to the Already Unfunded Pension Crisis

These enhancements increase the present value of future benefits, increasing unfunded liabilities. State contributions are already $5 billion below the actuarially determined levels; new promises would widen funding gaps and accelerate deterioration in funded ratios. Pension payments already account for one-fifth of the state budget, and adding tens of billions in additional obligations would further strain other essential services and raise borrowing costs over time.

The Safe Harbor Hypocrisy and Selective Sovereignty

The primary justification offered for these benefit increases is compliance with the IRS Safe Harbor provision. This federal rule allows public pension plans to exempt employees and employers from paying the full 12.4% FICA taxes into Social Security, provided the pension offers benefits at least as generous as a baseline Social Security replacement level.

Illinois eagerly complies with this federal mandate when it means expanding benefits supported by public-sector unions while also overriding local concerns (as in the Chicago police/fire bill). Yet when Truth in Accounting and others advocate amending the 1974 Employee Retirement Income Security Act (ERISA) to extend its proven minimum funding, transparency, and reporting standards to state and local public pensions, the same voices invoke “states’ rights” to block federal oversight.

This selective sovereignty is hypocritical: states accept federal rules that grow liabilities if those liabilities make them popular, but reject those that would require adequate funding and prevent benefit increases in severely underfunded systems. If ERISA’s standards applied today, Illinois’ recent and proposed pension benefit increases would be illegal, as they exacerbate an already precarious situation. ERISA’s exemption for public plans has been cited as a contributing factor to a nationwide $832 billion public pension shortfall, raising concerns about potential future federal bailout risk.

Why Pritzker’s Reform Window Makes This Especially Dangerous

In 2013, the SEC charged Illinois with securities fraud for misleading bond investors about pension risks. True reform demands full ADC first, stabilizing existing liabilities before creating new ones. Benefit increases do the opposite.

This is the moment for bipartisan discipline. Any Tier 2 discussion must begin and end with full ADC compliance and rigorous, independent cost analysis. And broader ERISA reform at the federal level would provide consistent accountability and remove politics from pension promises.

Truth in Accounting Urges Immediate Action

Illinois cannot afford to repeat past mistakes. Truth in Accounting calls on legislators and Governor Pritzker to:

-

Reject Tier 2 benefit increases.

-

Prioritize full ADC in every budget bill.

-

Determine the full cost of proposed pension increases to the state and local governments, and whether they can afford the related increased costs, before legislation is passed.

-

Enact TIA’s Fiscal Transparency and Accountability Act at the state level

-

Support amending ERISA to apply funding and reporting standards to public pensions.

The pension crisis was decades in the making, and Tier 2 benefit increases would make it dramatically worse for every local government across the state. Illinois taxpayers and retirees deserve fiscal reality over political expediency.